Industry & Market Highlights

Wishing you a wonderful Christmas holiday and a happy new year!

Housing supply will be the big story in 2020 – CREA

While Canadian housing suffered from relatively weaker sales in 2018 and 2019, the market will have to contend with the impact of shortages in housing supply next year, CREA stated in its latest forecast.

In the latest edition of its Resale Housing Market Forecast, the Canadian Real Estate Association predicted that the residential sector will enjoy sustained improvement into 2020, “with prices either continuing to rise or accelerating in many parts of Canada.”

Among the most important indicators is the fact that national economic activity is more than compensating for the weaknesses observed in the Prairies.

“The national resale housing market outlook continues to be supported by population and employment growth while consumer confidence is benefiting from low unemployment rates outside oil-producing provinces,” CREA stated. “Additionally, the Bank of Canada is widely expected to not raise interest rates in 2020.”

“The pillars strongly supportive of housing demand in Canada have remained intact: remarkable job creation, superior wage growth and a very low interest rates environment,” Lavoie explained. “The low and stable housing starts to labour force increase ratio is one of many metrics indicating no risk of over-building and refuting overblown concerns about the Canadian housing market.”

Combined with the sustained impact of the First-Time Home Buyer Incentive, these developments are paving the ground for a new year of accelerated housing activity.

“Recent national sales trends have improved by more than expected over the second half of 2019 while new listings have fallen. These trends have caused many housing markets to tighten, which has sharply lowered the national number of months of inventory,” CREA reported.

“In November 2019, this measure of the balance between supply and demand hit its lowest level since mid-2007. This is resulting in increased competition among buyers for listings and providing fertile ground for price gains.”

The national housing market saw muted price growth last month

The latest edition of the Teranet–National Bank National Composite House Price Index showed that Canadian home price growth in November has been slowed by declines and lack of movement in some major markets.

On a monthly basis, the Index went up by just 0.2% in November. This muted rise was largely due to the moderating influence of Halifax (down by 1.3%) and Winnipeg (down 0.6%), while Toronto, Victoria, and Ottawa-Gatineau remained relatively flat.

Miniscule gains were endemic, as seen in Edmonton (0.1%), Calgary (0.2%), Montreal (0.3%), Vancouver (0.4%), Hamilton (0.4%), and Quebec City (1.0%).

“For Vancouver it was a second consecutive gain after a run of 15 months without one. Home sales in that market have recovered from a March bottom to the average volume of the last 10 years,” the Teranet–National Bank joint report stated.

“The index for Toronto remains below its September peak. Its flatness coincides with a plateauing of home sales, not necessarily worrisome given that this market is balanced. The most sustained performer has been the Montreal urban area, whose index has risen in 17 of the last 20 months.”

However, these trends do not appear to have affected demand for housing product, with national sales volume posting its ninth consecutive monthly increase in November, and supply dropping to its lowest levels since 2007.

Data from the Canadian Real Estate Association showed that home sales nationwide increased by 0.6% month-over-month in November, and by 11.3% annually. New home listings fell by 2.7% from October to November, largely driven by scarcity in most of Ontario, as well as in Quebec and the Maritime provinces. By Ephraim Vecina.

Mortgage interest and meat are driving up the cost of living

The cost of living in Canada rose again in November according to the latest Consumer Price Index (CPI).

Statistics Canada said Wednesday that the CPI was up 2.2% year-over-year, building on the 1.9% rise in October. Excluding gasoline, it was up 2.3%, matching October’s increase.

Mortgage interest payments were up 6.6% from a year earlier – the largest percentage rise after auto insurance premiums (7.6%) – rents were up 3.1% and overall shelter costs rose 2.5%.

Meat prices gained 5.2% as demand for Canadian beef and supply-chain disruption pushed prices higher.

And energy costs were up 1.5% as gasoline increased by 0.9% year-over-year, its first rise since November 2018. This was in sharp contrast to the 6.7% year-over-year decrease in gasoline costs in October.

On a seasonally adjusted monthly basis, the CPI rose 0.1% in November, following a 0.3% increase in October with the cost of fresh vegetables the biggest increase at 8%.

The only province to escape an annual increase larger than was posted in October was British Columbia as the only province to see lower gasoline prices due to a surplus of fuel in the Pacific Northwest. By Steve Randall.

Why Canada’s ageing population should matter to you

This month’s economic letter looks at how Canada’s ageing population is changing our economy and how your business can benefit.

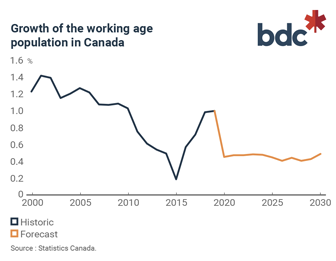

Canada is getting older. What does that mean in tangible terms? In the 1970s, there were eight Canadians of working age for each person older than 65. That number is now closer to four and is expected to fall to two by 2050. Ultimately, this means there will be fewer workers (in proportion to retirees) to drive economic activity and fund social programs.

Declining fertility rates and longer life expectancies explain Canada’s ageing demographics. Although immigration is helping to abate the impact of a low birth rate, growth in Canada’s workforce is expected to be much lower than in the previous decade at 0.5%.

The graph shows past and expected growth rates in Canada’s workforce. Note that low growth isn’t going to get better for a while.

What does an aging population mean for your business?

Labour Shortages: Is your company having trouble finding qualified employees? If yes, the situation is unlikely to get better any time soon because of our ageing population. The impact of labour shortages shouldn’t be underestimated. Research has shown that hard hit companies are more likely to experience lower growth, be less competitive and suffer a deterioration of the quality of their products and services.

BDC has a series of free and downloadable reports available on its website to help entrepreneurs deal with labour shortages. These reports provide tangible advice on how your business can automate production to overcome staffing issues; develop an employee value proposition to become a more attractive employer; and tap into under-utilized segments of the labour market, such as immigrants and Indigenous workers. You can download these studies here and here.

Consumption patterns: Some sectors will do better than others. Obvious winners include industries like health care, pharmaceuticals and home care that are needed to care for an ageing population. Travel and leisure businesses that offer “bucket list” type of experiences are also expected to do well.

Elsewhere, post-secondary institutions are also capitalizing on the trend by developing courses geared towards older adults. Referred to as the “University of the Third Age” (U3A), institutions are offering courses on such subjects as languages, philosophy, history and music that are specifically adapted to older adults.

Other sectors are likely to face more headwind. Research shows that older adults tend to buy higher quality goods and keep them longer. This will have an impact on consumption patterns and sales cycles in consumer products (think cars and appliances) and could represent an opportunity for manufacturers and retailers of higher-end, longer life brands.

Housing markets: Intuitively, you might think an ageing population would mean reduced demand for new housing. However, researchers at the Bank for International Settlement (BIS) argue that a shift towards an older population will actually increase demand for new homes.

The BIS argues that in wealthier countries, like Canada, the elderly will stay in their homes, given they generally own them outright and the stress associated with moving. This will tie up existing homes and new construction will be needed to satisfy demand from new buyers. Assuming the BIS is correct, the housing and construction sectors will benefit (at least in the short and medium term) from an older population.

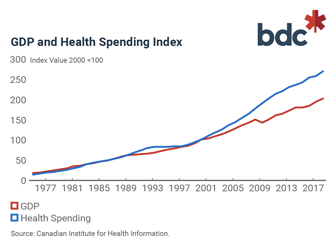

Impact on government spending: An ageing population will put upward pressure on government spending, notably for health care and pension costs. The graph, which plots the growth in health spending versus Canada’s GDP, shows that increases in health spending have outstripped economic growth since the early 2000s.

Furthermore, growth in the labour force is an important contributor to overall economic growth. Specifically, more people working translates into higher household income and spending. Conversely, an ageing population and shrinking labour force are likely to stifle growth. Slower GDP growth will have an impact on government tax receipts, adding to the burden from higher old-age related spending.

Governments are trying to mitigate the impact of the ageing population by encouraging greater workforce participation, increasing immigration levels and improving productivity through investments in machinery and enhanced worker skills.

If these solutions don’t suffice, governments will need to resort to heavier-handed solutions like raising taxes and the age at which you can collect government pensions. The funding burden will likely increase for consumers and businesses as someone will need to offset age-related government program expenses and fill the gap from lower income tax receipts.

Bottom line

The ageing of our population represents risks but also opportunities for small and medium-sized businesses. You should act now to position your business to respond to current demographic trends and maintain your growth. By BDC.

Prime Minister urges review of stress test

Minister of Finance Bill Morneau was urged to reconsider the borrower stress test in a Ministerial Mandate letter from Prime Minister Justin Trudeau.

The prime minister reiterated Morneau’s commitment to four key principles for the implementation of the government’s fiscal plan: reducing the government’s debt; preserving Canada’s AAA credit rating; investing in people and things that give people a better quality of life; and preserving “fiscal firepower” in the event of an economic downturn.

Among the list of top priorities were to “review and consider recommendations from financial agencies related to making the borrower stress test more dynamic.”

Whether or not anything comes of the recommendation remains to be seen, but some brokers are encouraged by the fact that the conversation is continuing.

“I think it’s definitely a step in the right direction and the fact that they’re even considering looking at it—especially after re-election—is a good sign,” said Michelle Campbell, principal mortgage broker at Mortgage District, based in Mississauga.

The stress test has somewhat begrudgingly been hailed as a success in terms of cooling overheated housing markets and making it more necessary for consumers to turn to mortgage brokers for guidance. There has been no shortage of criticism, however, due to the fact that it negates the purchasing power of first-time buyers as well as making it harder for those renewing mortgages to switch lenders and take advantage of better deals.”

“From my perspective, I don’t think that there shouldn’t be a stress test, but it should be reasonable.” Campbell sits on the chapter committee for MPC, which has asserted that a reasonable bar for a stress test would be .75 above the contract rate.

“The fact that they’re realizing that it it’s effecting first-time homebuyers the most, I think it’s a positive thing,” Campbell said.

The prime minister also indicated for Morneau to work with the Minister of Families, Children and Social Development who is the Minister responsible for the Canada Mortgage and Housing Corporation (CMHC) to further limit housing speculation by “developing a framework and introducing a 1% annual vacancy and speculation tax on applicable residential properties owned by non-resident non-Canadians. This would involve working with provinces, territories, municipalities and law enforcement to track housing ownership and speculation.”

Other priorities include a complete implementation of the new financial consumer protection framework and the introduction of legislation to “cut taxes for the middle class and those working hard to join it.” This tax cut would increase the basic personal income tax exemption by around $2,000 to $15,000.

Mandate letters are meant to outline the strategic priorities of each department and to enhance the transparency and accountability of government. Commitments are described in the mandate letters sent from the Prime Minister to each cabinet minister and represent action on top priorities identified by the government. Progress of the government commitments are then tracked by the Government of Canada. By Kimberley Greene.

Economic Highlights

Canada’s core inflation accelerates to highest in a decade, backing Bank of Canada’s rate break

Canadian underlying inflation hit the highest in a decade in November, reinforcing a decision by policy makers this month to refrain from cutting interest rates despite concerns around slowing growth.

Inflation rose 2.2 per cent in November from a year earlier, compared with 1.9 per cent in October, on higher shelter and vehicle costs, Statistics Canada reported Wednesday. The annual reading matched economist expectations. On a monthly basis, the consumer price index fell 0.1 per cent, also matching forecasts.

Core inflation — seen as a better measure of underlying price pressure than the headline figure — increased 2.2 per cent, the highest reading since 2009, from 2.1 per cent in October.

Wednesday’s report bears out the view from the Bank of Canada, which said in its December rate statement that inflation would increase temporarily in the coming months, due to year over year movements in gasoline prices.

“Should gasoline prices remain stable, the headline inflation rate should also cool back down in the second quarter of next year, as the year-ago comparisons become a bit firmer,” Royce Mendes, an economist at Canadian Imperial Bank of Commerce, wrote in a note. By Shelly Hagan.

Fitch: Canadian mortgage performance to remain stable in 2020

Canadian mortgage lenders shouldn’t worry too much about the performance of their loans in 2020 according to a new report from Fitch Ratings.

The firm says that performance should remain solid next year as strong employment, projected income growth, and low interest rates support mortgage performance across North America.

For Canada specifically, a slight increase to 0.3% is forecast, but this is near historic lows.

Canadian mortgage professionals may experience a sluggish pace though with Fitch calling for growth of just 1% due to affordability constraints and the continued impact of the B-20 lending restrictions.

With CMHC continuing to reduce its exposure to the market, smaller banks and non-bank lenders will find more financing challenges, reducing the overall availability of mortgage credit.

Home prices are expected to rise about 1% over the next two years on a nominal basis but real home prices will decline.

US mortgage market

By comparison, although the US mortgage market is supported by the same solid fundamentals of the Canadian market, Fitch expects arrears of at least 3 months to increase to around 1.5%, still low by historic standards.

The firm calls for US home price growth of 3%, just above CPI inflation, supported by solid job growth, a high household savings ratio and low mortgage rates, but tempered by slower GDP growth, cooling home prices in higher priced markets, and affordability constraints. By Steve Randall.

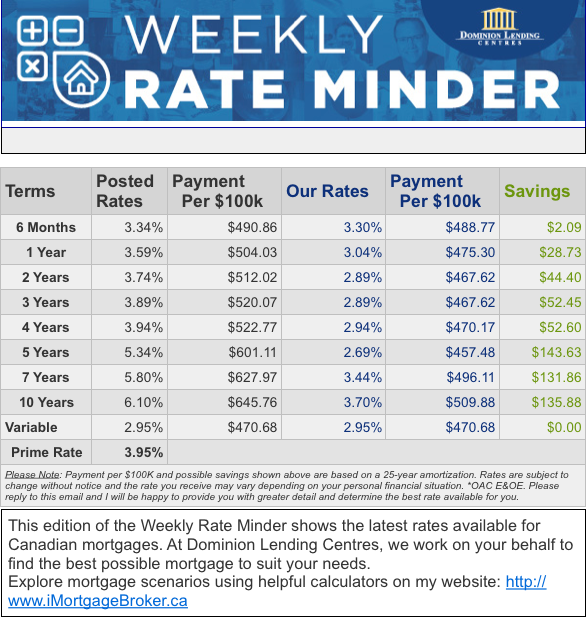

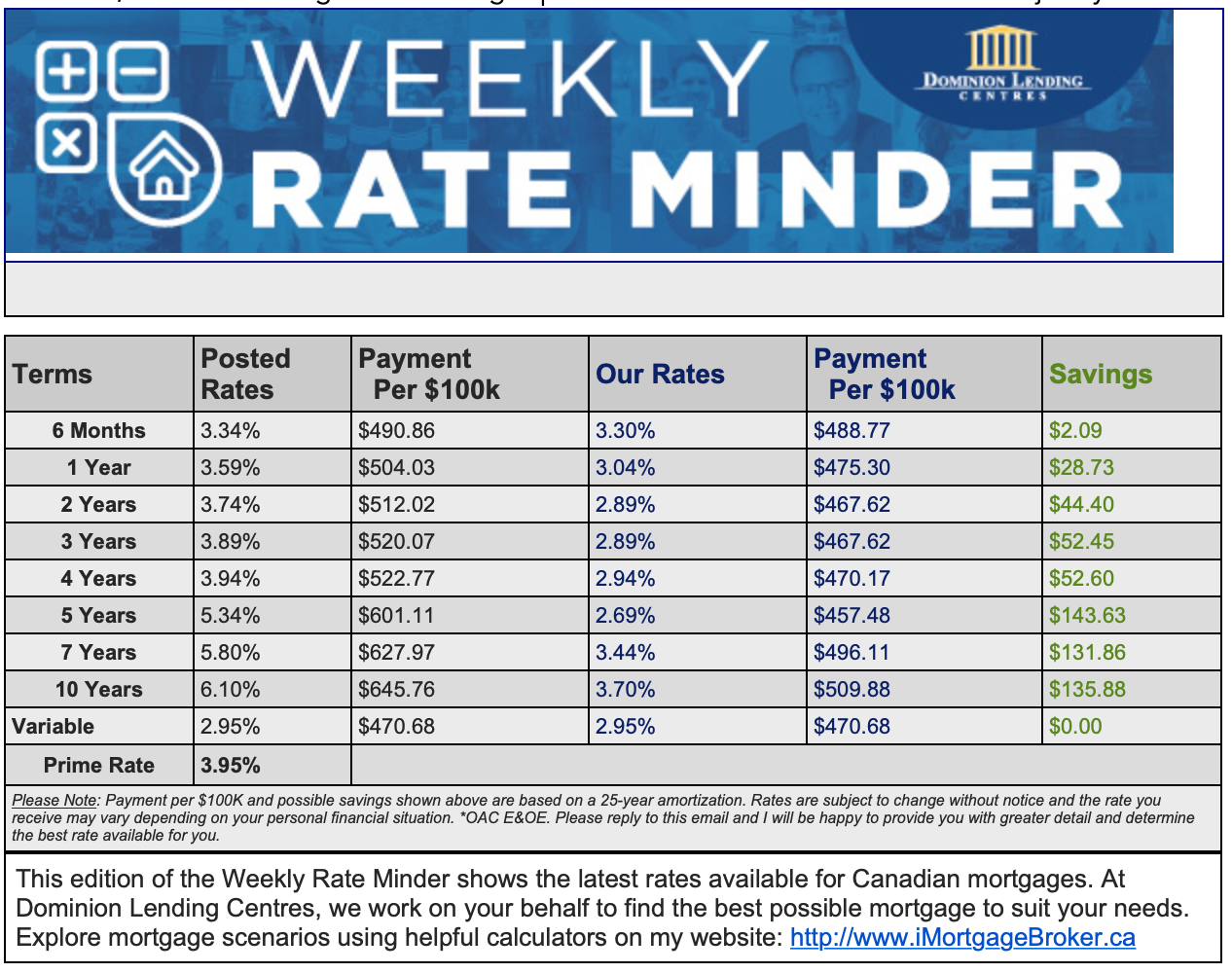

Mortgage Interest Rates

Prime lending rate is 3.95%. Bank of Canada Benchmark Qualifying rate for mortgage approval is at 5.19%. Fixed rates are creeping up to to pressure from increasing bond yields. Deep discounts are offered by some lenders for variable rates making adjustable variable rate mortgages somewhat attractive, but still not a significant enough spread between the fixed and variable to justify the risk for most.

Mortgage Update – Mortgage Broker London

There is never a better time than now for a free mortgage check-up. It always a great idea to revisit your mortgage and ensure it still meets your needs and performs optimally. Perhaps you’ve been thinking about refinancing to consolidate debt, purchasing a rental or vacation property, or simply want to know you have the best deal? Whatever your needs, we can evaluate your situation and help you determine what’s the right and best mortgage for you.

Adriaan Driessen

Mortgage Broker

Dominion Lending Forest City Funding 10671

Cell: 519.777.9374

Fax: 519.518.1081

415 Wharncliffe Road South

London, ON, N6J 2M3

Lori Richards Kovac

Mortgage Agent

Dominion Lending Forest City Funding 10671

Cell: 519.852.7116

Fax: 519.518.1081

415 Wharncliffe Road South

London, ON, N6J 2M3

Adriaan Driessen

Sales Representative & Senior Partner

PC275 Realty Brokerage

Cell: 519.777.9374

Fax: 519.518.1081

415 Wharncliffe Road South

London, ON, N6J 2M3