Industry & Market Highlights

The Benchmark Qualifying Rate Dropped from 5.04% to 4.94%

Announcement on Monday, May 25th from the Bank of Canada that the Benchmark rate dropped from 5.04% to 4.94%. This means that the average household income purchasing power has increased slightly and that you may qualify for on average $3k to $7k more in your maximum purchase price point. It is not going to make a large difference you your qualifying, but for many first time home buyer every little bit helps. Contact us for more information!

Housing market beginning to normalize after historically bad April: TD

Home sales dropped off a cliff in markets across Canada to what TD Senior Economist Brian DePratto called “historically depressed levels” in April.

It was enough to give most market observers whiplash as the year started on such an upbeat note that some commentators were even worrying that areas of the market were at risk of overheating during what was expected to be a blazing hot spring homebuying season.

But as the COVID-19 pandemic bore down on Canada, buyers began stepping to the sidelines before eventually being forced to do so by strict physical distancing measures introduced to curb the virus’ spread and the economic turbulence that came with it.

The result was a countrywide drop in sales activity last month that blew past any decline recorded during the 2008-2009 Global Financial Crisis for the worst for volume since 1984.

The enormity of the declines thankfully did not blindside housing market experts who had been predicting a huge, but temporary, hit to activity. And with April behind us, the market will now begin the steep, long climb back to some version of normalcy.

“With April in the rear-view, we can start talking about ever so tentative improvements in sales activity as provinces begin to gradually re-open their economies,” wrote TD’s DePratto in a research note late last week.

“We do expect sales to remain depressed for a few months longer as job markets slowly improve and buyers remain cautious, but a normalization process is likely already underway,” he continued.

DePratto’s counterpart on RBC’s economics team, Robert Hogue, issued a similar prediction that April’s activity levels would be as bad as things get for Canada’s resale housing market.

“Provinces are beginning to relax some restrictions—including Quebec earlier this week lifting its lockdown orders on the real estate industry—which will help house hunting function a little more normally going forward in parts of the country,” wrote Hogue in a note published Friday.

“Exceptionally low interest rates will also contribute to a gradual recovery taking hold in most markets across Canada,” he added.

Hogue went on to point out that the Canadian Real Estate Association, which released its grim April sales and pricing data on Friday, noted that it had already observed an uptick in sales and listings in its preliminary data for May. By Sean MacKay.

Residential Market Commentary – Downplaying dire doomsayers

As the Canadian economy starts its slow walk back toward normalcy, or towards whatever the new normal is going to be, Bank of Canada Governor Stephen Poloz is calling out the doomsayers.

With about a week to go before he steps aside on June 2, Poloz says he believes the economy is on track for a healthy recovery from the COVID-19 pandemic, starting in the second quarter of this year.

“Where we are today suggests we’re still tracking to our best-case scenario … not the dire scenario,” Poloz told reporters during a video roundtable last week.

“I do believe the… [pessimism]… I’m hearing is a little too dire. It’s a little overblown,” he said.

To Poloz’s way of thinking, too many forecasters are fixating on the collapse of the country’s GDP. But he points out that the underlying “behavioral adjustment” by people, the “downward spiral in confidence” normally associated with recession and depression is not occurring.

The Governor’s theory appears to be born-out, at least modestly, by the latest read on consumer confidence by the Conference Board of Canada. The figures for May show a 16 point increase in confidence from the record low of 47.5 hit in April.

The index now sits at 63.7 points. That is still 60 points below the pre-lockdown reading in February. But the numbers are also improving as Canadians look ahead. There is less pessimism about future finances and worries about future employment have also eased. By First National Financial.

Separating during the pandemic: What homeowners need to know

COVID-19 has impacted all sectors of the economy, including real estate. The uncertainty is particularly challenging for homeowners who are at a crossroad in their relationship or in the process of separating.

The heightened tension created by the pandemic can fuel anger and conflict, leaving children especially vulnerable. If it becomes too tense in the residence and someone needs to leave, the process has become a little more challenging than before, but there are still viable options.

Should homeowners sell when there is a separation during the pandemic?

At the time of writing, real estate remains a sellers’ market with little supply. It may be more difficult for families in need of alternative living arrangements to allow for a physical separation.

It is also challenging for couples to get an accurate value of their property because the markets are in such flux. Compounding this is the difficulty for a spouse to qualify for a mortgage if their income has been affected by a layoff or a termination as a result of the coronavirus. With such an overwhelming scenario and an uncertain economy, now may not be the best time to make important decisions such as selling the family home.

It may make more sense to access short-term rental accommodation during the pandemic while the legalities of the separation are sorted. The protocols for finding a rental property have changed to accommodate physical distancing, with virtual showings, and only people with serious offers may be able to attend in person to see the place before finalizing the offer to lease.

Consider the best interest of children

Couples struggle to know if it is in their children’s best interest to stay together under the same roof, even if there is a lot of acrimony, or if it’s better to live physically apart.

While it’s likely harmful to the children’s well-being if the family stays together under tense or acrimonious circumstances, there may also be harm to the children if a parent leaves without a formal parenting plan in place. Struggling parents should look for counsellors, lawyers, mediators and financial planners who now offer their services by phone or videoconference, to get quick, professional guidance toward the solutions that work best for the family’s circumstances.

Who pays what?

Money is often the biggest source of conflict, and this could get worse if someone’s livelihood was affected by the pandemic. They struggle to find a fair way to pay the household expenses and the children’s expenses after the decision to separate has been made – even if they continue to live under the same roof.

While there is no one-size-fits-all solution, there are many ways to deal with expenses. It depends on a number of factors, including who has financial resources. It may make sense to continue the same arrangements that were in place before the decision to separate until professionals can guide the family towards different arrangements.

In some cases, couples put an agreed amount of money in a joint account and use that to pay family expenses until there is a more long-term arrangement in place. Sometimes, separating spouses may even be able to structure their payments in a way that maximizes tax savings. It should be noted that if a couple decides to live in two separate residences during separation, these expenses are shared equally.

Family laws are fairly complex when it comes to finances and money, and it is recommended to speak to a family law lawyer or mediator about these types of questions.

Legal ways to separate

Among the various legal approaches, there are two very good options for separating families, and they are collaborative negotiations and mediation. These two systems are encouraged as the first choice under Ontario’s revised Family Law Act, to help families reach agreements out of court with the aim of preserving some kind of relationship after the legal process is complete. The cost also tends to be less than going to court.

Professionals that work in these two systems have received special negotiation and communication training, using specific techniques that are very beneficial to helping their clients and families.

Especially with courts closed during the pandemic, and only urgent matters being heard, collaborative negotiation and mediation offer fantastic avenues for couples to quickly access help and find solutions that are best for their family’s needs. By Nathalie Boutet.

OREA sets new ground rules for realtors as Ontario’s economy restarts

The Ontario Real Estate Association (OREA) has published its latest guidelines on home purchase transactions in the era of COVID-19.

“The health and safety of our realtors and their clients is OREA’s top priority during this pandemic,” said Sean Morrison, president of OREA. “As Ontario’s economy reopens, many Ontarians are looking to get back into the real estate market. Realtors are here to help make home buyers and sellers feel comfortable and safe while they work to find their dream home. OREA’s guidelines have been informed by up-to-date information from public health, best practices from the industry and experiences in jurisdictions across North America.”

OREA was among the earliest organizations to have petitioned a shift to mostly online transactions once the coronavirus pandemic took hold in late March.

“Now that the Ontario government has announced stage one of its plan to re-open the economy and with many consumers looking to get back into the market, it is important that realtors continue to help their clients feel safe and secure and keep the virus at bay,” OREA said in a statement this week.

The association is mandating its agents to “continue [using] virtual tools, conduct virtual open houses and virtual showings to the greatest extent possible,” despite the restarting of the economy. This includes maximizing the use of phone, email, and video communications with clients, as well as processing all documents via electronic channels.

Agents should also “thoroughly disinfect surfaces, leave doors open and keep lights on at all times during in-person showings,” OREA said. “When interacting with clients, maintain physical distancing and use personal protective equipment when distancing is not possible.” By Ephraim Vecina.

Pandemic disruptions won’t cause new home supply shortage: BMO

After a good showing in April, the team at BMO Economics is confident that home construction across Canada won’t see a major disruption due to the COVID-19 pandemic.

A report from the Canada Mortgage and Housing Corporation (CMHC) published late last week saw housing starts in April rise 11 percent over the same period last year despite the significant economic turbulence caused by the pandemic.

While starts still declined from March’s activity levels before the pandemic’s impact was fully felt, BMO Senior Economist Robert Kavcic called the home construction activity level “solid” amid shutdowns across many other sectors. Housing starts measure how many homes began construction during a given period and are generally viewed as a key factor in determining market health.

“Indeed, construction is one sector that appears to have skated through April with less damage than most, given softer restrictions and the ability to social distance on site,” wrote Kavcic in a research note.

With his relatively upbeat commentary, Kavcic joins fellow industry experts at TD and real estate consultancy Altus Group in predicting that home construction across the country would likely be less vulnerable to the disruptive effects of the pandemic than other sectors of the economy and even segments of the real estate industry.

Altus Group had published a projection last month that Canadian homebuilding would bounce back by July, but this was before the encouraging and prediction-defying April construction figures were published.

“One takeaway from this is that we’re not likely to see any material [housing] supply shortage coming out the other side, and the bigger risk for housing is that demand is more permanently depressed if the job market isn’t able to come back strongly,” wrote Kavcic.

The recession’s duration and the ultimate scale of the job loss caused by the virus are key questions economists have been grappling with when making predictions about the ability of the Canadian housing market to regain momentum after the worst effects of the pandemic have subsided.

Many in the industry, both in resale and new construction, are pinning their hopes on homebuyers sidelined during the crisis returning to the market in the late summer and fall, resulting in a late-year home sales rebound.

Those in the homebuilding industry have had plenty of reasons to celebrate so far this month with the better than expected housing starts data and the Ontario provincial government continuing to loosen restrictions on home construction activities.

But, as Kavcic pointed out, this is only one side of the supply and demand equation. By Sean MacKay.

Home sales fall, debt worries rise

The latest statistics from the Canadian Real Estate Association are stark but they should not be surprising. April sales hit a 36-year low, down nearly 57% from a month earlier and down almost 58% year-over-year.

As with March, though, average prices remained steady. Compared to a year ago the national average dipped 1.3% to just over $488,000. With Toronto and Vancouver taken out of the calculation the national average drops by nearly $100,000.

CREA points out that its composite Home Price Index shows an increase of almost 6.5% YoY.

The association is not offering any forecasts on sales or prices going forward.

As the COVID-19 pandemic continues to run roughshod through the housing market, the Bank of Canada is repeating its concerns about high household debt. The Bank sees the number of vulnerable households – those that put more than 40% of their income toward debt payments – increasing and falling behind on loan payments.

Calculations by the BoC indicate that up to one-in-five home-owning households do not have enough money to cover two months of expenses. One-third do not have enough to cover four months. Some 700,000 households have received deferrals, so far.

The central bank’s projections see the mortgage arrears rate climbing by about 0.8%, peaking next year when payment deferral plans offered by lenders start to expire. This is the Bank’s current, worst case scenario. The current mortgage arrears rate stands at just 0.2%. By First National Financial.

Key trends indicate slower housing market for rest of 2020

Flagging immigration numbers along with much-reduced purchasing power will pull down market activity for the rest of the year, according to the latest Teranet–National Bank of Canada House Price Index.

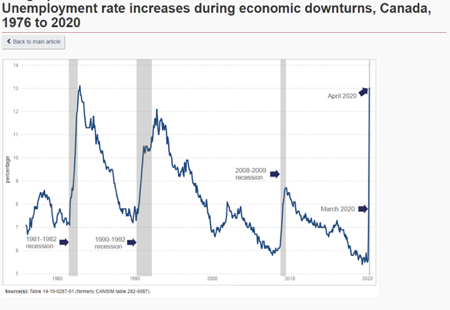

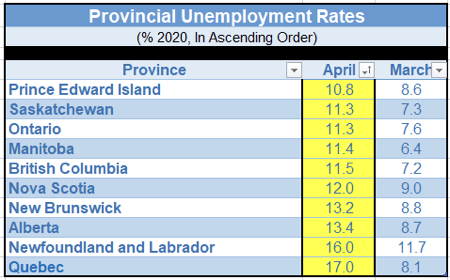

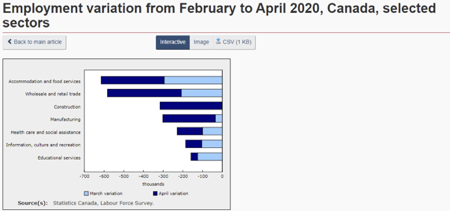

The steep climb in national unemployment numbers – from February’s 5.6% to 13% in April – will also have a significant influence in housing sales and values.

“In this context, demand for housing may decrease due to a reduction in immigration and would-be first-time homebuyers not being able to qualify for a mortgage loan,” Teranet said. “At the opposite, supply may be fuelled by homeowners unable to meet mortgage payments and for that reason will look to sell their home. In other words, a lasting high unemployment rate could mean downward pressure on house prices.”

The composite index in April was 5.3% higher than the same time last year. Ottawa-Gatineau (13.2% higher) imparted the most upward movement, along with Montreal (9.5%), Halifax (9.5%), Hamilton (8.9%), and Toronto (8.2%).

With the COVID-19 pandemic continuously savaging global markets, Canada Mortgage and Housing Corporation (CMHC) said that the pace of recovery will be markedly slow, with pre-recession prices returning only after three years.

“For Canada and for Ontario, I think, the best case we’re looking at … house prices getting back to their pre-recession levels, at the earliest, by the end of 2022,” CMHC Chief Economist Bob Dugan said. By Ephraim Vecina.

Household debt growth outstripping all other debt types

Over the last few decades, household debt growth accelerated faster than every other debt class, according to real estate information portal Better Dwelling.

Citing data from the Bank of Canada, the analysis said that the trend “makes Canadian households [among] the most vulnerable” globally.

“In 2000, household debt was just 58% of GDP. By the end of 2019 Q4, that number has hit 100% of GDP,” Better Dwelling said. “This is amongst the highest of advanced economies.”

BoC numbers indicated that national household debt hit a peak of $2.28 trillion in March, increasing by 0.44% from February and 4.6% from March 2019. Outstanding mortgages accounted for $1.64 trillion of this sum, rising by 0.49% monthly and 5.3% annually.

The impact on monthly budgets was inevitable: Even before the COVID-19 pandemic took hold, Canada’s insolvency incidence was already at 11,575 filings as of February, which was the highest level since 2010.

The Office of the Superintendent of Bankruptcy Canada said that this volume was 9% higher on an annual basis. Ontario posted the greatest increase during that month, at 3,837 filings (up 16.8% year over year), with Quebec’s 3,770 filings (up 1.9% annually) coming in at a close second.

“[These figures] underscore how vulnerable Canadian households are to income interruption. Over the next few months we’ll likely see an unfolding of two crises: the global pandemic and the bursting of the Canadian consumer debt bubble,” MNP LTD president Grant Bazian said. “Many households were already limited in their ability to face any kind of financial disruption. Now, all Canadians are feeling the effects on their paycheques, pocketbooks and stock portfolios. Those who were already saddled with a lot of debt are in economic survival mode.” By Ephraim Vecina.

Expect rapid post-pandemic recovery – BoC’s Poloz

Despite multiple headwinds and the continuous ravages of COVID-19, Canadian market activity and purchasing power will be able to recover quickly after the outbreak eases, according to outgoing Bank of Canada Governor Stephen Poloz.

“We have to be able to manage the risks around those things, so I’m not going to dismiss [the worst scenarios],” Poloz told BNN Bloomberg. “But, me personally, I do think on balance what I’m hearing, the flow that I’m hearing, is a little too dire, a little bit overblown.”

In the greater scheme of things, the coronavirus will not be a fatal roadblock, Poloz said. While the national economy is still on track to decline at least 15% this year, “you should see a very rapid return to production” once the economy restarts in late 2020, he said. “I’m relatively optimistic, what I find, compared with what the talk is.”

These predictions dovetailed with other observers’ forecasts of speedy post-pandemic recovery across the board, pointing at the Canadian financial system’s robust fundamentals.

However, the pace of this recovery will depend on homeowners not selling their assets, according to TD Economics.

“Absolutely key to our forecasts is the assumption that listings mirror sales by dropping substantially in the near term and recovering gradually thereafter,” said TD economist Rishi Sondhi. “This puts a floor on prices and sustains relatively tight supply-demand balances across most markets, allowing for the resumption of positive price growth as provincial economies are re-opened.” By Ephraim Vecina.

Why does CMHC’s Evan Siddall think Canada is headed for a ‘deferral cliff’?

In comments delivered to the Standing Committee on Finance on Tuesday, Canadian Mortgage and Housing Corporation CEO Evan Siddall laid out a potentially bleak scenario for the country’s homeowners. Siddall told parliamentarians that by September, if Canada’s economic recovery fails to generate enough momentum, 20 percent of mortgages could be in arrears.

“A team is at work within CMHC to help manage a growing debt ‘deferral cliff’ that looms in the fall, when some unemployed people will need to start paying their mortgages again,” Siddall said during the Committee’s videoconference. “As much as one fifth of all mortgages could be in arrears if our economy has not recovered sufficiently.”

It was one of many disturbing claims made by Siddall, who also told the Committee that the nominal house price in Canada could fall by as much as 18 percent over the next six to 12 months, with the biggest losses expected in oil-driven economies like Alberta and Saskatchewan and in overheated markets like Toronto. If prices fall by 10 percent, Siddall said first-time buyers could lose as much as $45,000 on a $300,000 home.

But the deferral issue didn’t seem to phase him.

“Canadians do a very good job of paying their mortgages, even when they’re under water, so our loss forecasts are not extreme,” he said in an exchange with Progressive Conservative MP Pierre Poilievre. When asked by Poilievre for CMHC’s potential loss forecast, Siddall estimated that it could be as high as $9 billion.

According to DLC’s Dr. Sherry Cooper, Siddall’s claim that 20 percent of mortgages could be delinquent by September borders on the ridiculous.

“It’s kind of bizarre to me,” she says. “Most economists are finding fault with it.”

An arrears rate of 20 percent would essentially mean that the Bank of Canada’s efforts to ensure the availability of credit and the federal government’s pumping of billions of dollars into the economy to prevent business closures and forced bankruptcies will actually accelerate the rate at which Canadian mortgages are turning sour.

“The Bank of Canada estimates that the delinquency rate could possibly move up from .25 percent to .8 percent. And now we’re talking about 20 percent delinquency rates?” Cooper says. “Give me a break.”

When asked if there was a possibility that Siddall was referring to deferrals when he used the word “arrears”, Cooper was doubtful.

“No, he’s a very smart guy,” she says, despite the unlikelihood of his prediction.

“It’s not going to happen. The highest delinquency – which is what ‘arrears’ is – rates we’ve ever seen in history are nowhere near [the projected 20 percent],” she says.

Centum FairTrust owner Jimmy Hansra agrees with Cooper’s assessment.

“The government has been pretty proactive in terms of providing as many programs as they possibly can to weather the storm,” he says, adding that there’s “no way” Siddall’s arrears projection is accurate.

“Even his comments about CMHC seeing housing prices falling by 18 percent I think are overblown, too,” says Hansra. “Nobody knows what’s happening with house prices.”

Hansra isn’t preparing for the kind of worst-case scenario Siddall laid out. Instead, he says his team is readying themselves for a potential, although still unlikely, stream of borrowers looking for refinancing or equity take-out solutions that will require private money.

“I don’t see it happening,” he says, “But if it does, I think that’s the only way mortgage professionals are going to be able to provide financing for their customers. Because if they’re not going to be able to make their mortgage payments and they have equity sitting in their home, either people are going to look to use home equity lines of credit to make those payments or they’ll look for some sort of second or third mortgage financing.”

Hansra stresses that projections like Siddall’s, particularly when they’re made at a time with no parallel in human history, need to be taken with a few million grains of salt.

“It’s all a guess,” he says.

If CMHC did envision a 20 percent arrears rate by fall, a fair question to ask, says RateSpy founder Robert McLister, is why they are not acting now to mitigate what would be an utter catastrophe for the Canadian economy.

“I think that if the government really thought there was going to be 20 percent arrears, they would take action,” McLister says. “You can’t have one in five homeowners not paying their mortgage, with a large percentage of those leading to liquidation. You know what that would do to home prices. You know what that would do to the economy. It’s not going to happen.” By Clayton Jarvis.

Stress test 2.0? What a 10% minimum down payment requirement would mean for Canadian buyers

Canadian Mortgage and Housing Corporation CEO Evan Siddall’s recent address to the Standing Committee on Finance contained a plethora of negative projections, from housing prices falling by 18 percent to one-fifth of all Canadian mortgages being in arrears by September. But it was his comments around the advantages of making 10 percent down payments and CMHC’s attempts to limit demand that have the industry wondering if an increase in the minimum down payment requirement may be in the cards.

As Siddall made his case for the approaching “deferral cliff”, a scenario where unemployed homeowners who have deferred their mortgage payments are asked to start making them again despite not returning to work, he shared with parliamentarians two key pieces of data that associate five percent down payments with increased risk.

The first, a chart that tracks the percentage of loans in deferral by their loan-to-value ratios, showed that 69 percent of the mortgages currently in deferral fall into the 90-95 percent LTV category. The implication seems to be that if there were fewer borrowers putting down five percent, the deferral cliff Siddall described might be less towering.

Siddall singled out first-timers again when he discussed the potential losses they could face if housing prices fall by 10 percent.

“Unless we act, a first-time homebuyer purchasing a $300,000 home with a 5 per cent down payment stands to lose over $45,000 on their $15,000 investment if prices fall by 10 per cent,” Siddall’s statement read. “In comparison, a 10 per cent down payment offers more of a cushion against possible losses.”

Because CMHC will be on the hook for any insurance claims triggered by failing mortgages, Siddall also said the Corporation is evaluating its underwriting policies.

“So if housing affordability is our aim, as surely it must be, then there must be a limit to the demand we help to create, especially when supply isn’t keeping up,” he said.

That’s the same logic that gave Canada its mortgage stress test. Many brokers are worried that a 10 percent minimum down payment would have a similarly chilling effect on business

Few in the industry seem to think the change is imminent. Either way, the discussion around down payment levels has shone a harsh light on the anxiety-ridden situation facing first-time buyers. By Ephraim Vecina.

Re/Max challenges CMHC home price projections

Housing industry players are opposing Canada Mortgage and Housing Corporation’s dire forecast of an 18% decline in home prices over the next 12 months, claiming that demand remains elevated and inventories continue to hover near record lows.

“Assuming that demand continues its current course, Canadian real estate prices will likely remain relatively stable or experience a single-digit price correction at worst,” RE/MAX said, adding that its agents are still reporting multiple offers on a regular basis.

“CMHC doesn’t seem to understand the sheer number of sellers that would have to accept this kind of price reduction, in order for average housing prices to plummet to this degree in such a short time span,” said Christopher Alexander, executive vice president and regional director with RE/MAX of Ontario Atlantic Canada. “Sellers simply won’t accept that kind of discount on their listings. A statement of this nature is panic-inducing and irresponsible.”

Government agencies should instead focus on how the housing markets – and the Canadian financial system as a whole – could weather the unprecedented impact of the coronavirus, according to the C.D. Howe Institute.

“Ottawa and the provinces need to recommit to fiscal and monetary anchors in light of the unprecedented stimulus response provided by all levels of government and the Bank of Canada throughout the COVID-19 crisis,” C.D. Howe said. “Canada is emerging from the first wave of the pandemic with very high public and private debt loads and is increasingly dependent on domestic and foreign investors to finance them. With the loss of Canada’s fiscal anchor, maintaining investor confidence so that public and private debt can be carried at a reasonable cost is essential.” By Ephraim Vecina.

![]()

Mortgage Interest Rates

Fixed mortgage rates have been dropping steadily in the past two weeks with fixed rates right back at historically low levels. Variable rates discounts deepened only slightly. View rates Here – and be sure to contact us for a quote to help you find the lowest rate for your specific needs and product requirements.

The Bank of Canada’s target overnight rate is 0.25%. Prime lending rate is 2.45%. What is Prime lending rate? The prime rate is the interest rate that commercial banks charge their most creditworthy corporate customers. The Bank of Canada overnight lending rate serves as the basis for the prime rate, and prime serves as the starting point for most other interest rates. Bank of Canada Benchmark Qualifying rate for mortgage approval is 4.94%.

![]()

Your Mortgage

If you have concerns about your mortgage and the rapidly changing market, please contact us to discuss your needs, concerns and options in detail to protect your best interest.

Ensure that your current mortgage is performing optimally, or if you are shopping for a mortgage, only finalize your decision when you are confident you have all the options and the best deals with lowest rates for your needs.

Here at iMortgageBroker, we love looking after our clients’ needs to ensure you get all the options and the best deals and best results. We do this by shopping your mortgage to all the lenders out there that includes banks, trust companies, credit unions, mortgage corporations & insurance companies. We do this with a smile, and with service excellence

Reach out to us – let us do all the hard work in getting you the best results and peace of mind!

We encourage you to follow guidelines from our public health authorities:

Middlesex Health Unit

https://www.healthunit.com/novel-coronavirus

Southwestern Public Health

https://www.swpublichealth.ca/content/community-update-novel-coronavirus-covid-19

Ontario Ministry of Health

https://www.ontario.ca/page/2019-novel-coronavirus

Public Health Canada

https://www.canada.ca/en/public-health/services/diseases/coronavirus-disease-covid-19.html

Factual Statistics Coronavirus COVID-19 Globally:

https://www.worldometers.info/coronavirus/

https://gisanddata.maps.arcgis.com/apps/opsdashboard/index.html#/bda7594740fd40299423467b48e9ecf6