Industry & Market Highlights

Home prices have some support despite sales slowdown – RBC Economics

The national market can still provide some impetus for home price growth despite declining sales, according to Royal Bank of Canada Senior Economist Robert Hogue.

“Prices are determined by both demand and supply. What we saw in March is that supply came down quite a bit as well,” Hogue said in the April 15 edition of the 10 Minute-Take podcast by RBC Economics. “Sellers in this kind of turbulent environment have decided to wait it out, or maybe they have changed their minds, because they might not get the full value of their property under these conditions.”

Robustness as a fundamental feature of the housing sector was also observed by Royal LePage. Hogue said that while the market couldn’t conduct business as usual due to the pandemic, there were still some notable bright spots.

“In markets like Toronto and Montreal, for instance, prices continued to accelerate relative to February,” Hogue said. “Now, we don’t think that markets will necessarily sustain that kind of acceleration, but nonetheless, the point is that there is still quite a bit of support for prices despite plummeting activity.”

However, Hogue warned that both Toronto and Vancouver might see steeper market declines in April, and that the long-term value of Canada’s homes will depend heavily on the duration of the slowdown.

“Our assumption is that the economy starts to open up again sometime in June. Prices are probably going to stay relatively flat in most cases.” Hogue said. “If lockdown measures and the recession last longer than expected, downward pressure on prices are going to build up across the board.” By Ephraim Vecina.

Residential Market Commentary – March madness

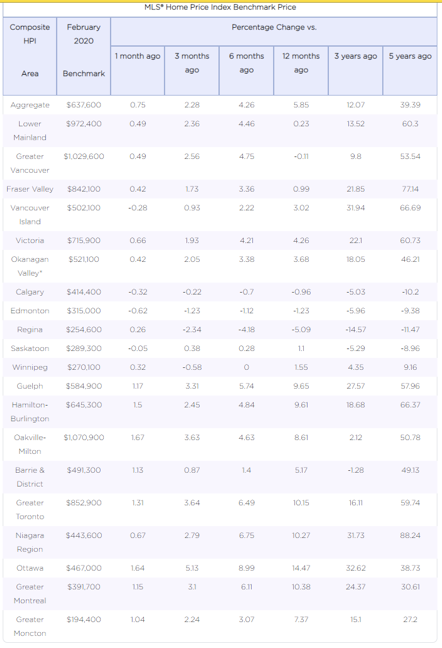

The national home sales numbers for March have been delivered by the Canadian Real Estate Association. As expected, they show the promising start to this year’s spring buying season has come to an abrupt end.

Earlier CREA released sales figures for Toronto and Vancouver, the country’s biggest and busiest markets. They showed those cities going into a tailspin in the second half of the month. Nationally, the market followed suit.

Here is a quick look at the country’s biggest markets:

Greater Toronto Area: -28%

Montreal: -13.3%

Greater Vancouver: -2.9%

Calgary: -26.3%

Edmonton: -13.2%

Winnipeg: -7.3%

Hamilton-Burlington: -24.9%

Ottawa: -7.95%

CREA’s early numbers for April suggest more of the same. Prices, though, are standing pat.

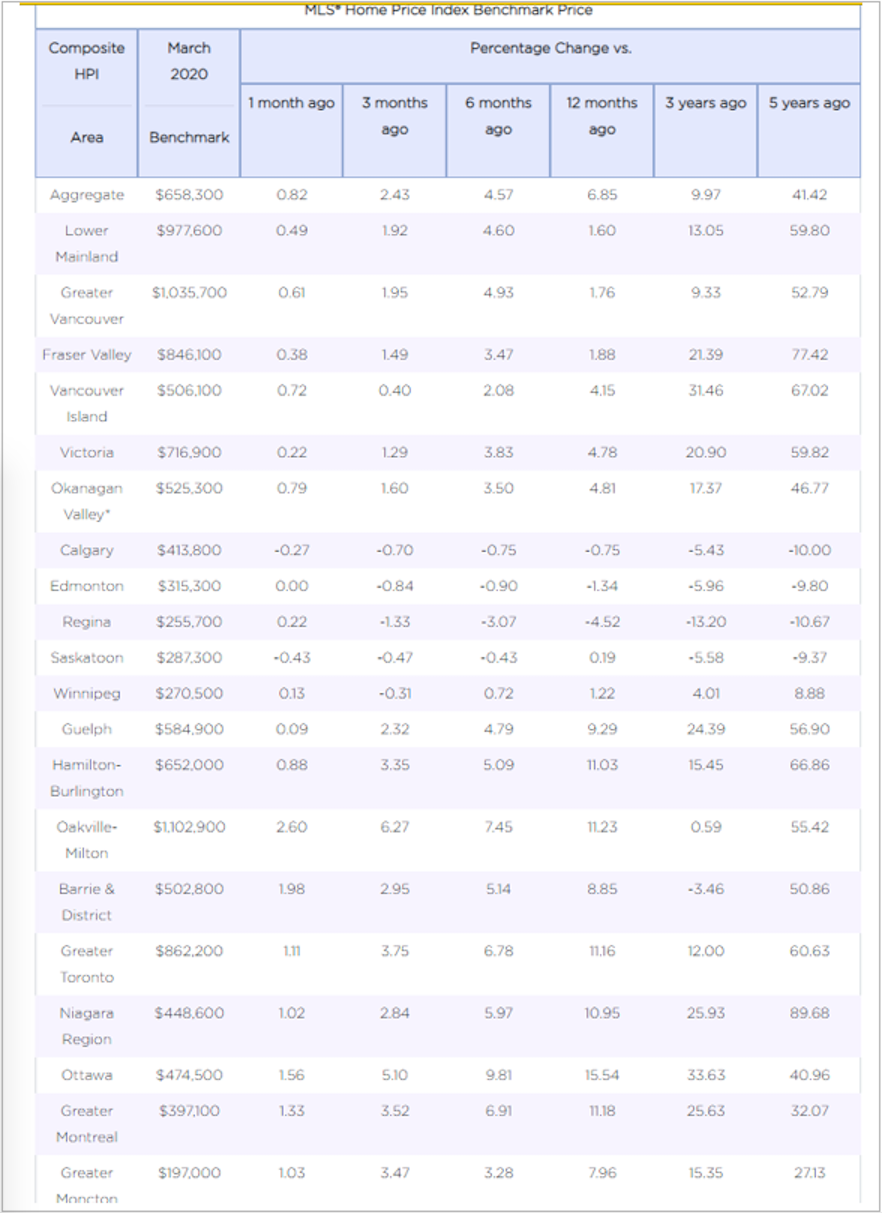

Generally, market watchers believe prices are holding steady because of a significant drop in new listings. They were down 12.5% in March, compared to February. The MLS Home Price Index rose 0.8% m/m and is up almost 7.0% compared to a year ago. These are early statistics and April’s final results will likely give a better indication of what is in store.

Analysts will also be watching the bankruptcy and default numbers. Increasing levels of unemployment and income loss, due to COVID-19 measures, could push debt laden households over the edge, forcing them to put their homes on the market. Any surge in that kind of activity could well lead to price declines. By First National Financial.

Reduced purchasing power more apparent in Canada’s largest markets

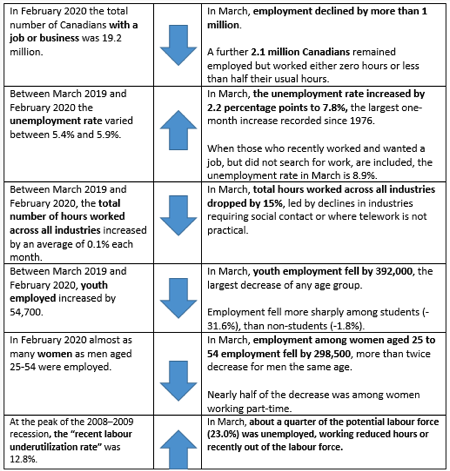

Unemployment has a disproportionate impact on the country’s largest housing markets, according to new Statistics Canada figures.

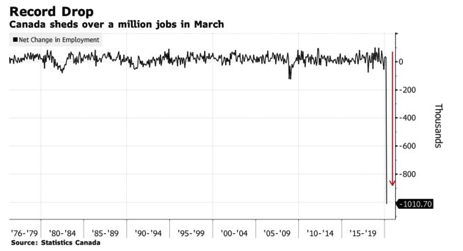

Across Canada, the employment sector declined by 5.3% from February to March, representing more than 1 million lost jobs. The unemployment rate rose to 7.8%, spurred by a record high 2.2% monthly increase.

Of particular concern is the sharp drop in employment in the private sector (down 6.7%), which was at a rate nearly double that of the public sector (down 3.7%).

“Unemployment increased by 413,000 (+36.4%), largely due to temporary layoffs,” Statistics Canada said. “In addition, the number of Canadians who had worked recently and wanted to work, but did not meet the official definition of unemployed, increased by 193,000.”

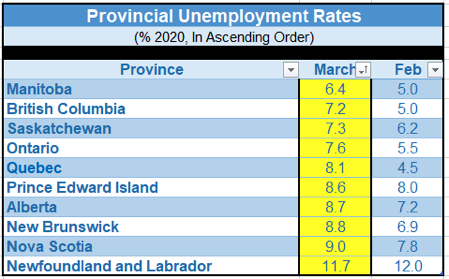

The agency’s March figures also indicated that unemployment rates in Toronto, Vancouver, and Montreal have experienced rapid increases last month.

The trend is compounding the already severe socio-economic effects of the COVID-19 pandemic, according to real estate information portal Better Dwelling.

Toronto’s unemployment rate stood at 7.8% as of March, having grown 11.42% annually. Meanwhile, Vancouver saw its share of unemployed workers shoot up by 68.89% year-over-year to reach 7.6% – a sharp about-face from the numbers traditionally associated with the city’s robust labour sector.

Of the top housing markets, Montreal suffered the highest unemployment rate last month, increasing by 51.67% annually to end up at 9.1%. By Ephraim Vecina.

First-time homebuyers suffering massive job losses during pandemic: Altus

Canadians in the typical first-time homebuyer age range were hit with full-time job losses that neared 200,000 in March when compared to employment levels just a month prior.

Real estate consultancy Altus Group used recent figures from Statistics Canada’s Labour Force Survey and its own internal data to assess the impact that the COVID-19 pandemic may have on future homebuying activity in Canada.

First, Altus Group mined its own recent data on first-time homebuyer demographics across the country. It found that Canadians between the ages of 25 and 44 made up 84 percent of first-time homebuyers over the last two years according to Altus Group data. The narrower 25 to 34-year-old segment made up the majority, with 64 percent of first-time homebuyers falling into this age range.

The firm then reviewed Statistics Canada’s preliminary data on job losses that came as a result of COVID-19’s spread across the country. It observed that 108,000 full-time jobs were lost in the 25 to 34-year-old range while 77,000 were lost in the 35 to 44-year-old range. Of course, losses were felt across all age ranges, with under-24s seeing the largest percentage decline when compared to the previous month and the 45 to 54-year-old age group rivalling the total job losses seen in the 25 to 34-year-old range.

That being said, potential first-time homebuyers are likely to be more adversely affected by job loss when it comes to their future ability to purchase a home. Older groups typically have more savings and a previously purchased property to leverage, while younger groups have yet to enter their prime homebuying years. Potential first-time buyers in the 25 to 44-year-old range — especially those at the younger end of the spectrum — are counting on this time to save for a downpayment and enter the market.

“These job loss patterns could have implications not just for absolute housing demand levels going forward, but also the relative mix of demand between the various segments (for example, first-time buyer, move-up buyer, move-down/lifestyle and “younger” senior segments),” wrote Altus Group in a post titled ‘Massive job losses among key potential first-time homebuyer age groups’ that was published recently on its website. By Sean Mackay.

‘Buyer’s market’ for renters may change the rules for Canada’s residential real estate: Don Pittis | CBC News

There is nothing so bad that it does not end up helping someone is the old saying, and while the COVID-19 outbreak is bad for pretty well everyone, long-suffering renters may finally get a break.

Newly unemployed gig workers and real estate investors will be collateral damage, but experts in the property market are already observing what may be an inflection point in a trend where rents have gobbled up an increasing share of young workers’ incomes.

Already, there are early signs that while the supply of rental properties continues to grow, demand has slumped, even in Canada’s hottest property markets, such as Vancouver and Toronto. And while the demand for housing will likely eventually resume its climb, there are reasons to expect the decline in rental prices will outlast the immediate economic effects of the coronavirus.

That’s partly because the market was already showing signs of strain and was due for a readjustment. Like other sectors of Canadian real estate, the sudden economic downturn will expose faults in a rental market dependent on high levels of borrowed money.

‘Swimming naked’

The quote from world-famous investor Warren Buffet that “only when the tide goes out do you see who is swimming naked” may turn out to apply in this case.

A report on Friday from property analysts Urbanation showed that while the 2020 rental market started the year strong, there were already early signs of a slowdown in rental price increases. But with the arrival of COVID-19, that slowdown transformed into an absolute rental price dip.

“As demand fell faster than supply in the second half of March, rents experienced a slight decline,” said the report. “The average monthly rent in the post-COVID-19 period decreased 0.7 per cent year-over-year.”

Rental-focused construction is at a 50-year high, and while demand is falling sharply amid the outbreak, once started, projects are hard to stop.

People like Hilliard MacBeth, long-time financial analyst and author of When the Bubble Bursts, have repeatedly warned that the over-leveraged Canadian property market was merely waiting for something to prick it with dangerous results for the whole economy. The Bank of Canada has said stress testing has shown Canada’s financial system can take the heat.

Nonetheless, a report last week by business news service Bloomberg that Canadian property “once safer than gold” is heading for a reckoning was widely retweeted and sent shivers through the real estate sector.

And it is clear that not just ordinary Canadians up to their eyes in debt from a mortgage on their own home are suffering. Banks have also been deferring the mortgage payments of rental property owners, prompting objections from those who blame short-term rentals, in particular, for soaring house prices and rents.

“Should someone with four properties really be granted financial assistance?” Steve Saretsky, a Vancouver real estate agent asked in the Bloomberg report.

There are plenty of signs that a plunge in tourism has already upset the shortest of rentals of the type offered by Airbnb hosts. And mortgage deferrals are not free money if the banks continue to charge interest on the amounts landlords invested in hope of earning a profit.

Good for renters, not for landlords

But one well-respected adviser to the private sector property market has warned that pain for landlords is not over.

“All this is going to hit the rental market first,” says Ben Rabidoux, who runs North Cove Advisors, an information service for the professional residential real estate market. Of course, a warning to landlords of falling rents will be good news for renters.

In one respect, Rabidoux is far less gloomy than some about the home resale market overall, saying defaults remain unlikely so long as the economic meltdown caused by COVID-19 is less than six months.

But the real estate insider says there are strong signals that just as the supply of rental properties is hitting a peak, the number of people wanting to rent is falling.

The devastated Airbnb market, down about 95 per cent, is only part of it. Unemployed gig workers and students are moving in with relatives. Immigration has slowed to a trickle.

And Rabidoux’s research shows that the influx of non-permanent residents, including foreign students and people on work permits to fill gaps in Canada’s tight labour market, both of whom depend on the rental market and normally about 200,000-strong, has gone into reverse.

“We have a 50-year high in rental units under construction and a 50-year high in completions of those rental units coming online,” says Rabidoux. That’s over and above the current flood of condos built to sell to Canadians as rental investment properties. And once underway, he says, those projects will continue to inundate the market over a two-year timeline.

While people who have bought homes to live in them will be less affected, falling rental prices will inevitably impact other parts of the market, convincing some to rent rather than buy, said Rabidoux.

“You’re going to see it bleed into the resale market three, six, nine months down the road,” he said.

But for anyone renting, maybe now is the time to start shopping around. By Don Pittis.

COVID-19 creating legal issues for sellers

With just over a week until rent cheques are due, the blizzard of rent and mortgage deferrals that hit the Canadian housing market on April 1 is expected to blow in once again.

While most landlords at this point have come to some understanding with their tenants regarding late or adjusted rent payments, RealEstateLawyers.ca senior partner Mark Weisleder says there is no shortage of other issues his clients are still coming to grips with when it comes to selling their homes.

“It’s tough for everybody,” Weisleder says.

One question Weisleder has been repeatedly asked involves what to do when a sold property’s rental occupants express an unwillingness to vacate, ostensibly because of the restrictions COVID-19 has placed on their ability to either work or locate a new place to live.

Multiple sellers approached their tenants in February with 60-day notices to vacate, which allows them to stay in place until the end of April while giving the property’s new owners until May to take possession. But with the 60-day period now elapsed and the world stumbling collectively through an economic concussion many of these tenants are choosing not to leave.

According to Weisleder, sellers in this predicament have few options.

“You can’t evict them because the Board is closed down,” he says, estimating that the backlog of cases due to clog up Ontario’s Landlord Tenant Board could last up to a year. “You have to work something out. Work with the tenant – maybe find them another place to live – otherwise you’re going to have to extend your deal. Or maybe pay the buyer an incentive to just assume the tenant for as long as it takes.”

Weisleder says there have also been cases where buyers have been refused access to their new properties by the current rental tenants, even though the seller has agreed in writing to allow them into the property.

“They have the right,” he says of the tenants. “It’s safety.”

With 44% of Canadian households reporting some form of work disruption, there will inevitably be a number of potential buyers forced to abandon their plans mid-deal. The consequences could be dire for any buyers who agreed to purchase a property only to see their finances go up in smoke weeks later.

Weisleder points to the instant dip the Ontario market experienced following the 2017 Fair Housing Plan as a parallel. Prices and appraised values plummeted, forcing a rash of buyers, whose financing plans fell apart, to back out of deals to which they had already agreed.

He recalls a specific case where a set of buyers had put down a $50,000 deposit on a property only to walk away from the deal because of an inability to get the purchase financed. The sellers wound up selling the home for $500,000 less than what had been agreed to. After being taken to court, the buyers were ordered to make up the difference and pay the sellers the full $500,000.

Regardless of the excuse, whether it be sickness or quarantine or an inability to access capital, buyers cannot walk away after they have agreed to purchase a property.

“If they don’t close and a settlement is not reached, the seller can sue them,” Weisleder says.

But there are similar cases when legal action may not be the proper play for sellers. If a first-time buyer puts down five percent but ultimately walks away from a deal because of a lack of funds, the option to sue exists, but Weisleder questions the value such a step would have for the seller, who would be accruing $30,000-40,000 in legal fees for the privilege of suing someone who has no money.

He suggests that sellers in this case may be better off negotiating further with their buyers, possibly agreeing to the smallest price reduction possible that would still allow them to secure financing.

“For a seller, with these buyers, that’s a good deal,” he says.

The high number of calls Weisleder is fielding should provide comfort for anyone watching the Ontario housing space. The high volume of requests for assistance illustrates just how alive the market was prior to the arrival of COVID-19.

“Most deals,” Weisleder reminds us, “are closing.” By Clayton Jarvis.

Real Estate Services COVID-19 legal update on support services

REALTORS® services were deemed essential by the Province. But it’s not business as usual. Real estate was deemed essential so Realtors could continue to serve clients who were closing transactions or who urgently needed to sell or buy property.

On that note, we have received many questions about whether or not the essential business designation extends to include photographers, videographers, stagers, cleaners and home inspectors.

To help guide our Members during this incredibly challenging time, OREA has obtained a legal opinion on whether photographers, videographers, stagers and cleaners (referred to as “Service Providers” in this email) can provide services to REALTORS® given that Ontario has ordered all places of business to close, except those on the ‘Essential Business’ list (referred to as the “Order”).

Home Inspectors have received their own legal opinion and the Ontario Association of Home Inspectors has advised that “OAHI’s corporate counsel has confirmed home inspections are still essential ‘in the context of a real estate transaction process…’” during the State of Emergency. Their letter can be found here.

Here’s what you need to know:

Yes, Service Providers such as photographers, videographers, stagers and cleaners may generally be able to do what they need to do at the Seller’s home in support of a real estate transaction.

Service Providers would fall within the “Essential Business” category of Supply Chain businesses that supply another Essential Business, namely the real estate agent services. However, at least the following steps are required:

- The REALTOR® (and not their client) contracts with and retains the Service Provider’s services;

- Especially in the case of videographers, cleaners and stagers, the REALTOR® has appropriately contracted with their client to provide the client with those services;

- Only people absolutely necessary attend; and

- All other Emergency Orders and laws are followed (e.g. no more than 5 persons on the property etc.) including local public health authority guidelines.

This is based upon Ontario’s Emergency Orders in place April 9, 2020. As the COVID-19 situation is constantly changing, please note that the rules can change at any time.

Most importantly, because the condition and characteristics of the property, the market and the specific contracts a REALTOR® may have with both the Service Provider and their client are unique and the behaviour of both the Service Provider and REALTOR® are also contributing factors, this document can only act as a ‘general guide’. An absolute answer requires consideration of all of these factors on a case-by-case basis.

Finally, the responsibility rests with the Service Providers to comply with any Emergency Orders and the law when providing their services. A REALTOR® should not instruct the Service Provider to do anything a Service Provider does not consider to be legal.

For more information please see a summary of the detailed analysis here. By Sean Morrison, President, Ontario Real Estate Association.

Economic Highlights

Residential Market Commentary – Crumbling confidence

The latest consumer confidence numbers from the Conference Board of Canada are another dull spot on an already gloomy outlook.

The April survey by the policy think-tank suggests the future outlook of debt-laden Canadians is at an all-time low and the plunge happened at a record pace – 73 points in just two months. By comparison, the financial collapse of 2008 also saw a 73-point drop, but that took 13 months.

The Conference Board survey indicates 36.1% of respondents expect to see their finances deteriorate over the next six months. That is 14 percentage points higher than the previous record of 22.1%. The survey also suggests a majority of Canadians have a grim view of future employment with 53% of respondents saying they expect their job prospects to get worse over the next six months.

This pessimism is affecting spending plans, at least in the near term. More than three-quarters of those surveyed, 76.5%, say this is a bad time to make a major purchase like a vehicle or a home. That is more than 20 percentage points higher than the previous record, posted in February, 2016.

The Conference Board’s readings seem to be confirmed by government figures that show a sharp drop in inflation, a spike in unemployment and a jump in insolvencies. Nationally, filings for personal and business bankruptcies and proposals rose 9% in February, compared to a year earlier – even before the coronavirus pandemic really took hold. (Consumer filings led the way with a 9.2% increase. Business filings were up 1.9%.). By First National Financial.

Head of CFIB: “Tens of thousands” of businesses will close in wake of COVID-19

In recent comments to Bloomberg, Canadian Federation of Independent Business president Dan Kelly predicted the damage done to the economy by measures to slow the COVID-19 pandemic will spell the end for an obscene number of businesses.

Kelly said on Wednesday that, even with the assistance provided by government support programs, he sees “no scenario under which there are not tens of thousands of permanent business closures.”

It’s an alarming projection, but according to BMO chief economist Doug Porter, Kelly’s estimate is reasonable.

“Those numbers seem quite realistic,” Porter told MBN in an email. “I would point out that in a typical year, there are often as many as 140,000 new businesses created in Canada and almost that many that “exit” every year. That is by no means to downplay the figure, and there will no doubt be plenty of hardships among small businesses.”

A series of weekly surveys conducted by the CFIB illustrates growing anxiety among the Federation’s members. The most recent data show that 80% of businesses are either partially or fully closed because of COVID-19, an increase of approximately 27% over the past four weeks.

That lack of business has left a gaping hole where revenues should be. The CFIB survey found that 55% of respondents have experienced a decrease in gross sales revenue of at least 50% since the outbreak of COVID-19. As of April 16, the average amount the extended disruptions have cost respondents was $203,461.

(Interestingly, 44% of respondents said they are unsure if their businesses will survive if current conditions are kept in place until the end of May, yet only 36% have tried to apply for the Canada Emergency Business Account.)

Just how many of these impacted businesses wind up going broke remains to be seen. But if Kelly’s prediction is even marginally accurate, it will mean fewer businesses turning to lenders for funding.

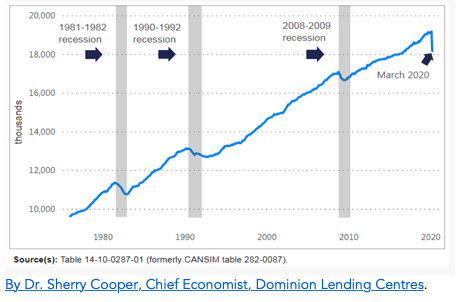

“As far as the lending space is concerned, certainly loan losses will rise,” says DLC’s Dr. Sherry Cooper, who stresses the uncertainty of the current situation. “Banks and other lenders are already increasing reserves for these losses. How much these losses will be depends on how long this lasts.” By Clayton Jarvis.

Debt, unemployment compounding market threat of COVID-19

Mounting household debt and unemployment risk are likely to have a dangerous domino effect on the national market, according to a senior bank official.

“I think it’s been really tough on people, not just financially but mentally – there’s just so much stress in the system,” said Laura Dottori-Attanasio, head of domestic banking at Canadian Imperial Bank of Commerce. “That stress will continue to build until we get a little more clarity about what happens next and when it happens.”

“We do have a highly indebted Canadian consumer that we’ve been talking about for quite some time, and just under half of Canadians live paycheque to paycheque,” Dottori-Attanasio told BNN Bloomberg.

A recent report by the federal government’s Parliamentary Budget Officer (PBO) indicated that the unemployment rate was at 7.2% as of the end of the first quarter. This is likely to worsen significantly in the coming months: 14.8% in Q2, 15% in Q3, and 12.7% in Q4, with the year-end rate pegged at 12.4%.

MNP LTD’s late-March survey also found that 49% of Canadians are just $200 or less away from insolvency. Another 46% said that they are anxious about their current debt levels, while 34% fear for the stability of their employment.

Dottori-Attanasio said that the greatest threat in the near future is the accumulated stress on a consumer base already burdened by uncertainty surrounding the COVID-19 pandemic.

“If you add that people are no longer working and generating cash flow, I do think it makes for a toxic combination that’s going to be much more difficult to overcome the longer this takes to resolve,” Dottori-Attanasio said. By Ephraim Vecina.

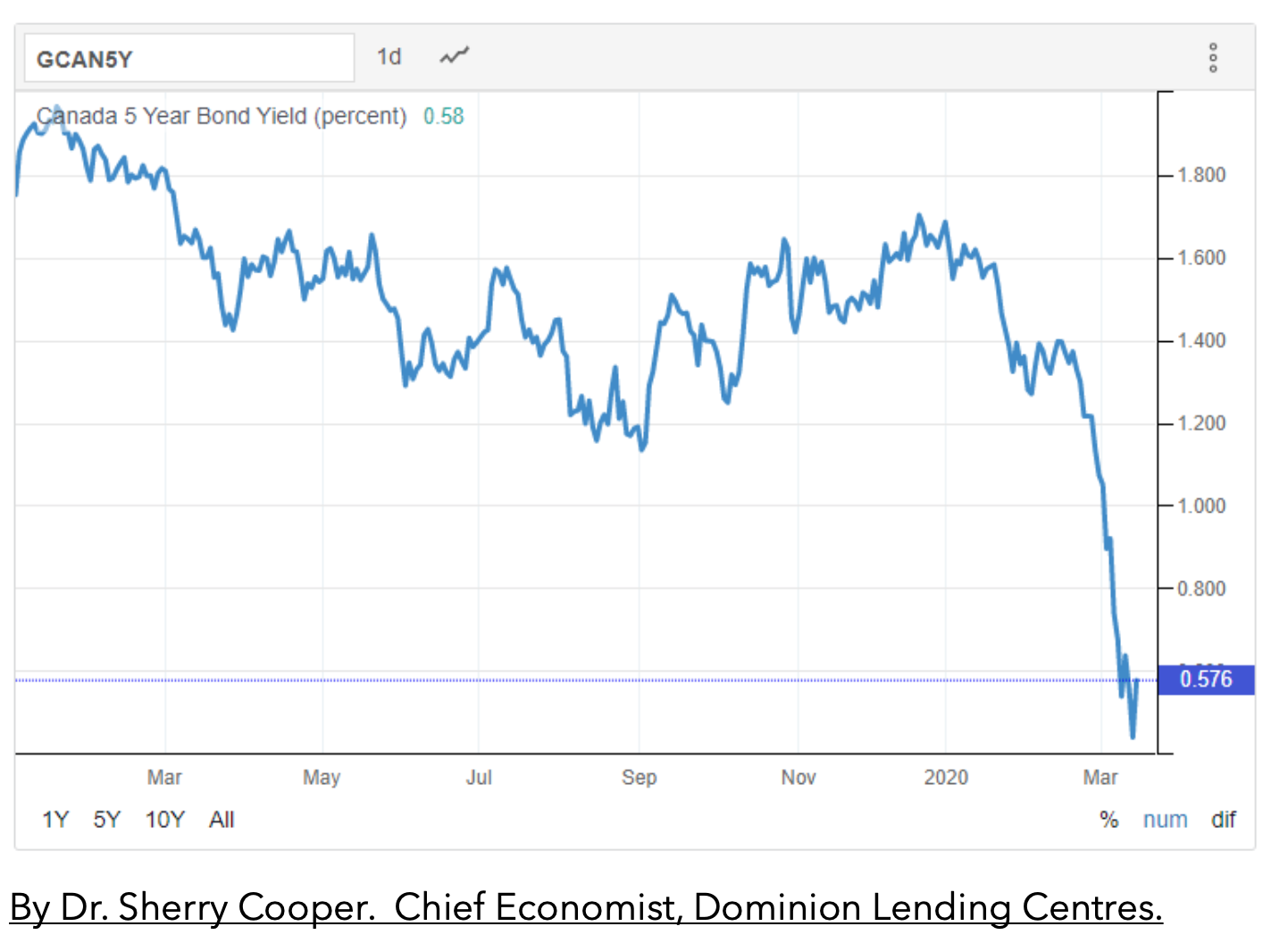

Mortgage Update – Mortgage Broker London

Mortgage Interest Rates

Fixed mortgage rate movement has stabilized and levelled out in the past week as lenders get more familiar with the new normal during uncertainty and as bond markets stabilized more. Variable rates have also responded the same way. Some lenders are using this opportunity to take market share for more competitive pricing and a slight drop in rates. View rates Here – and be sure to contact us for a quote to help you find the lowest rate for your specific needs and product requirements.

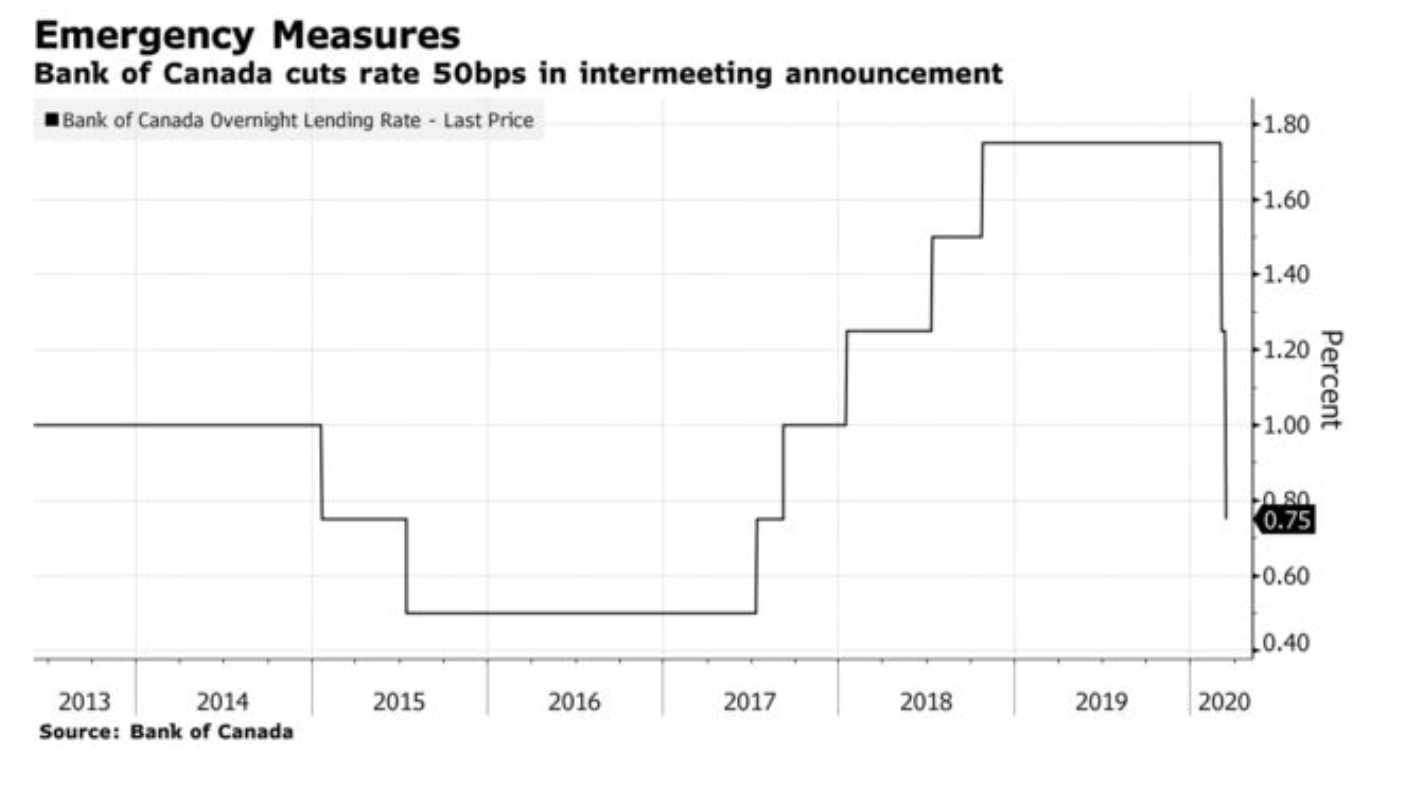

The Bank of Canada’s target overnight rate is 0.25%. Prime lending rate is 2.45%. What is Prime lending rate? The prime rate is the interest rate that commercial banks charge their most creditworthy corporate customers. The Bank of Canada overnight lending rate serves as the basis for the prime rate, and prime serves as the starting point for most other interest rates. Bank of Canada Benchmark Qualifying rate for mortgage approval is 5.04%. Changes to the mortgage qualifying rate is coming into effect April 6, 2020: Instead of the Bank of Canada 5-Year Benchmark Posted Rate, the new benchmark rate will be the weekly median 5-year fixed insured mortgage rate from mortgage insurance applications, plus 2%. Read the Government of Canada Department of Finance summary on Benchmark Rate for Insured Mortgages statement here.

Mortgage Update – Mortgage Broker London

Your Mortgage

If you have concerns about your mortgage and the rapidly changing market, please contact us to discuss your needs, concerns and options in detail to protect your best interest.

Ensure that your current mortgage is performing optimally, or if you are shopping for a mortgage, only finalize your decision when you are confident you have all the options and the best deals with lowest rates for your needs.

Here at iMortgageBroker, we love looking after our clients’ needs to ensure you get all the options and the best deals and best results. We do this by shopping your mortgage to all the lenders out there that includes banks, trust companies, credit unions, mortgage corporations & insurance companies. We do this with a smile, and with service excellence!

Reach out to us – let us do all the hard work in getting you the best results and peace of mind!

We encourage you to follow guidelines from our public health authorities:

Middlesex Health Unit

https://www.healthunit.com/novel-coronavirus

Southwestern Public Health

https://www.swpublichealth.ca/content/community-update-novel-coronavirus-covid-19

Ontario Ministry of Health

https://www.ontario.ca/page/2019-novel-coronavirus

Public Health Canada

https://www.canada.ca/en/public-health/services/diseases/coronavirus-disease-covid-19.html

Factual Statistics Coronavirus COVID-19 Globally:

https://www.worldometers.info/coronavirus/

https://gisanddata.maps.arcgis.com/apps/opsdashboard/index.html#/bda7594740fd40299423467b48e9ecf6

]

]