![]()

Market Commentary

Climbing home sales suggest a soft landing. The October read on home sales and prices has returned words like “balance” and “soft landing” to the conversations of market watchers.

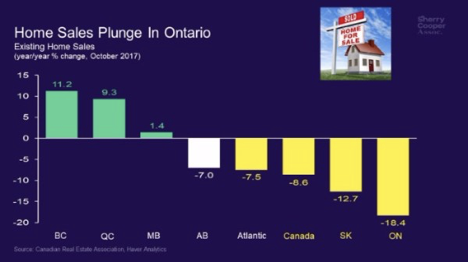

The Canadian Real Estate Association reports home sales edged up 0.9% in October compared to September, for a third straight month of gains. But sales were down 4.3% from a year ago. The national average price of a home was up 5% to just shy of $506,000 y/y. Once again the Toronto and Vancouver areas skewed prices higher. Factoring out those markets brought the average price down to $383,000.

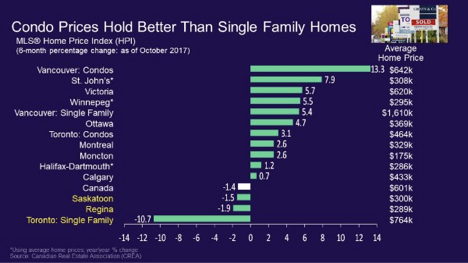

The Teranet Home Price Index recorded a 1% drop in October, the 2nd monthly decline in a row. Toronto led the way in the Teranet report with a 2.8% drop. Five of 11 markets monitored for the index recorded declines.

The CREA figures show new listings in October were down 0.8% from September while the sales-to-new-listings ratio was up 1% to 56.7%. That falls inside the 40% to 60% range that is considered balanced. The national inventory of housing stands at five months, which is in line with long term averages. By First National Financial LP.

New National Housing Strategy

The federal Liberals’ all new National Housing Strategy was unveiled with great fanfare on National Housing Day (Nov. 22) last week. It is big on promises and grand numbers. But that kind of political flash and glitter make it hard to see the dull, but important, details of how the strategy will actually work.

The first-of-its-kind strategy formally makes housing a human right in Canada and is slated to cost $40 billion over 10 years. Among its grand goals:

– Construction of up to 100,000 new affordable housing units

– The repair of 300,000 affordable housing units

– Cutting “chronic homelessness” by 50%

There are several other pledges, each with its own impressively big number.

It is all very laudable and it is deemed necessary right across the political spectrum. The problem, though, is the lack of detail. One veteran Parliament Hill reporter who attended the technical briefing prior to the announcement has commented that technical questions were often answered with “details to be determined”.

There have also been warnings that Ottawa has not laid out any clear measures of success for the strategy. Former Parliamentary Budget Officer Kevin Page says cities, which will actually spend the money, will be reporting results based on their own criteria and without any context. He says Ottawa has to get the right information in order to make sure the strategy is working.

And in a particularly cynical move a key component of the strategy – a rent subsidy called the Canada Housing Benefit – will not kick-in until 2020, after the next federal election.

Market Statistics by CMHC

CMHC has just published the latest Rental Market Report for Canada. In the Report, we use data from our Rental Market Survey to identify current trends on Canada’s rental markets. We also identify differences observed between data from October 2016 and data from October 2017.

Results from this year’s Survey show:

•a 0.7 percentage point decrease in the overall vacancy rate for purpose-built rental units (dwellings that were built with the intention of supplying the rental market); and

•a 0.3 percentage point decrease in the overall vacancy rate for rental apartment condominiums in the secondary rental market (dwellings that were initially built to supply the owner-occupant sector, but whose owners rent them out).

Here are some key findings:

Vacancy rate for purpose-built rental units

Data for this group are drawn from all centres with a population of at least 10,000 individuals, including major urban centres across Canada.

Overall, the vacancy rate for this group decreased from 3.7% to 3.0%. An increase in supply of only 1.2% represented a significant decrease in growth compared to the previous year. At the same time, demand remained steady. Key factors sustaining demand included high levels of net international migration, improving employment conditions for younger households, and the ongoing aging of the population.

Change in Vacancy Rates for Purpose-Built Rentals, by Province, from 2016 to 2017

|

Province

|

2016 (%)

|

2017 (%)

|

Change (%)

|

|

New Brunswick

|

6.6

|

4.1

|

-2.5

|

|

Quebec

|

4.4

|

3.4

|

-1.0

|

|

Prince Edward Island

|

2.1

|

1.2

|

-0.9

|

|

Alberta

|

8.1

|

7.5

|

-0.6

|

|

Ontario

|

2.1

|

1.6

|

-0.5

|

|

Nova Scotia

|

3.0

|

2.6

|

-0.4

|

|

Manitoba

|

2.8

|

2.7

|

-0.1

|

|

Saskatchewan

|

9.4

|

9.3

|

-0.1

|

|

British Columbia

|

1.3

|

1.3

|

0.0

|

|

Newfoundland and Labrador

|

6.5

|

6.6

|

0.1

|

Vacancy rate for secondary rental units

The secondary rental market consists largely of rented condominium apartments. Data for this group are drawn from 17 major centres across Canada.

The overall condominium vacancy rate declined from 1.9% to 1.6%. Just like for the purpose-built rental market, this reflected stronger growth in demand than in supply. On the secondary market, however, these dynamics were true everywhere except in Saskatoon, Ottawa and Vancouver, where supply exceeded demand.

Rents increased

In terms of rental costs, low vacancy rates tended to correlate with higher rental costs.

As well, we compared the average rent for two-bedroom rental condominiums and two-bedroom purpose-built apartments (in the same 17 centres in which we surveyed rental condominiums). This average rent was lower for purpose-built apartments ($1,044) than for rental condominiums ($1,421). No doubt a key factor is that rental condominiums are typically newer and tend to offer a greater range of amenities.

Economic Highlights:

United States

· It was an eventful week across financial markets, with a plethora of economic data, Fed speeches, and political developments keeping investors busy.

· Domestic economic data was robust and beat expectations. Following on hurricane-induced weakness previously retail sales, housing starts and industrial production get a significant boost from rebuilding efforts in October. Recent data suggests that GDP growth was over 3% in Q3 and is tracking near 3% during Q4 — helping reduce economic slack.

· Diminishing slack should provide comfort for the Fed to raise rates in December — a view highlighted by several FOMC members this week. The hike is further supported by recent CPI and PPI data which was stronger than expected.

Canada

· Economic indicators this week remained consistent with our view that economic activity is holding at an above trend pace in the second half of 2017.

· Headline inflation weakened in October as energy prices reversed previous gains. Underlying inflation indicators were little changed. Nevertheless, strong economic activity and rising wage growth all suggest that inflation will trend higher.

· Downwardly revised estimates of the Canadian neutral policy rate released by the Bank of Canada suggest less room for conventional policy to offset future economic shocks or increases in financial stability risks.

Rates

No change to primer lending rate currently at 3.2%. Bank of Canada Benchmark Qualifying rate for mortgage approval is at4.99%. No change in fixed rates. No change in variable rates.

Other Newsworthy

Tips on Using Social Media Successfully

A large part of a real estate agent’s job is to keep in touch with clients. The best real estate agents I have seen in my 40 years of experience do a fabulous job at this. With the growth of technology, social media is a great tool that allows agents to engage with clients. However, most agents are using it incorrectly in their strategy. They don’t understand why people use social media. Let me show you what they’re doing wrong and how you can improve to boost your earnings.

Most real estate agents don’t know why they’re on social media! They believe that it is a big microphone where they scream at their clients to get attention for their business. These agents constantly post content to try and show how much they know about the industry. If this is what you are doing, you must stop using social media immediately.

Now, you’re probably thinking, how could this be? Why isn’t posting and sharing content our main priority on social media? This is because the key to using social media is to engage with your clients. Most agents are doing the total opposite. I am not saying that posting isn’t important but what you should focus on is responding to clients. As you build your network on social media, you will need to spend more time engaging.

Think of social media as a big networking party. No one wants to talk to the person who is constantly ranting and raving about how great they are. Instead, you gravitate towards someone who is genuinely interested in what’s going on in your life. On social media you must engage your clients the same way. You should like their photos, comment on their posts and try to engage in conversation with them. For example, if you see your client post a picture of their son’s basketball game, you can comment and ask what the score was. These small touch-points add up and it will help you grow your relationships with clients.

Every time someone comments, likes or shares your post it releases dopamine. This is the chemical in your brain that makes you happy, like when you sell a listing! Engaging with the clients and making them happy is important. Now that I have explained all of this, let’s revisit our original question. Why are we on social media? The answer is we want to stay top of mind with our clients.

The key to having a long-term, great career is to create and maintain a client database. Within that database, every client knows about three to five people who are going to buy and sell real estate. Are these people thinking of you when they are buying or selling real estate? If not, you will be losing a ton of business and they will go with another agent. Staying top of mind keeps you relevant and gives you the opportunity to get referrals.

Now that you understand social media, you need to develop a plan on how to use it. What works for me is I set up four sessions in the day when I check my social media. Every session consists of 10 minutes where I engage with clients. I focus my efforts on using just two social media platforms. This allows me to achieve my goals of interacting with clients while not spending too much time online. The platforms that work best for agents are Facebook and Instagram. If you are just starting to use social media now, begin with these two.

The real estate industry is about keeping in touch and staying top of mind. Use the tactics that I have shown you and you will see a difference in your returns. Social media is a complex tool, but in the technology age you must adapt, or you will be left behind. By Alex Pilarski

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Please Note: Payment per $100K and possible savings shown above are based on a 25-year ammortization. Rates are subject to change without notice and the rate you receive may vary depending on your personal financial situation. *OAC E&OE. Please reply to this email and I will be happy to provide you with greater detail and determine the best rate available for you.

This edition of the Weekly Rate Minder shows the latest rates available for Canadian mortgages. At Dominion Lending Centres, we work on your behalf to find the best possible mortgage to suit your needs.

Explore mortgage scenarios using helpful calculators on my website: http://www.iMortgageBroker.ca

- We are Canada’s largest and fastest-growing mortgage brokerage!

- We have more than 2,600 Mortgage Professionals from more than 350 locations across the country!

- Our Mortgage Professionals are Experts in their field and many are ranked among the best nationally.

- We work for you, not the lenders, so your best interests will always be our number one priority.

- We have more than 100 mortgage programs, making it easy to choose the best fit for your unique situation.

- We close loans in all 10 provinces and 3 territories.

- We can process your mortgage in as few as 7 days.

- We are the preferred mortgage lender for several of Canada’s top companies.

- Dominion Lending Centres’ Mortgage Professionals are available anytime, anywhere, evenings and weekends – and we’ll even come to you!